Jade Lizard Option Strategy: Setup, Risk Profile & Profit Zones

Master the jade lizard option strategy: a neutral-to-bullish credit spread with no upside risk. Learn strike selection, margin, Greeks, and when to deploy this income play.

Why the jade lizard exists: fixing the short strangle's biggest flaw

A trader sells a strangle. Premium collected: $4.50. The stock rallies 18% in three days. Loss: $2,300. The upside call explodes, the downside put expires worthless, and the trader's account takes a hit that wipes out six weeks of premium collection.

The jade lizard solves this exact problem. It's a three-leg credit spread that eliminates upside risk entirely while keeping the high probability and premium collection of a short strangle. You sell a put, sell a call, and buy a further out-of-the-money call to cap the upside loss at zero. If the stock rockets, your max profit is locked in. If it drops, you have defined risk. If it stays flat, you collect the full credit.

This strategy works when implied volatility is elevated but you expect the stock to stay neutral or drift higher. It's not a beginner play—you need to understand vertical spreads, margin requirements, and how to adjust multi-leg positions under pressure.

What you'll learn:

- How the jade lizard eliminates upside risk while keeping high credit

- Strike selection formulas for the short put, short call, and long call

- Margin requirements and capital efficiency compared to short strangles

- When to deploy jade lizards vs iron condors or short puts

- Python code to calculate breakeven, max profit, and profit zones

- Common mistakes that turn a neutral trade into a directional disaster

What is a jade lizard option strategy

A jade lizard is a three-leg, neutral-to-bullish options strategy that collects a net credit with no upside risk. You simultaneously:

- Sell an out-of-the-money put (short put)

- Sell an out-of-the-money call (short call)

- Buy a further out-of-the-money call (long call)

The credit you collect from the short put and short call must exceed the width of the call spread (short call strike minus long call strike). This ensures that even if the stock rallies to infinity, your max loss on the call spread is less than the total credit received, resulting in a guaranteed profit at expiration if the stock finishes above the short put strike.

The jade lizard is a variant of the short strangle, modified to remove upside risk. It's structurally similar to a big lizard (which uses a call credit spread and a short put), but the jade lizard specifically refers to the setup where the call spread width is narrower than the total credit.

Key characteristics:

- Net credit received at entry (typically $2.00–$5.00 per contract on mid-cap stocks)

- No upside risk: max profit is the credit received, regardless of how high the stock goes

- Downside risk: defined by the short put strike minus the credit received

- Breakeven: short put strike minus net credit

- Ideal conditions: elevated IV, neutral-to-bullish outlook, stock trading in a range

Strike selection: building the three-leg structure

Selecting strikes for a jade lizard requires balancing credit received, probability of profit, and margin efficiency. The goal is to collect enough premium that the call spread width is fully covered, with additional credit left over for profit.

Step 1: Choose the short put strike

Start with the short put. This is your primary risk zone. Select a strike with a delta between 0.20 and 0.30 (20–30% probability of finishing in-the-money). For a 45-day expiration, this typically places the strike 1–2 standard deviations below the current price.

Example: Stock trading at $150. The $140 put (delta 0.25) sells for $2.80. This gives you a 75% probability the stock stays above $140 at expiration.

Step 2: Choose the short call strike

Select a short call with a delta between 0.15 and 0.25. This should be above the current stock price, reflecting a neutral-to-bullish bias. The short call generates additional credit but introduces upside risk that you'll cap in the next step.

Example: The $160 call (delta 0.20) sells for $2.00.

Step 3: Choose the long call strike

Buy a call further out-of-the-money to cap your upside risk. The width of this call spread (short call strike minus long call strike) must be less than the total credit received from the short put and short call combined.

Example: The $165 call costs $1.10. Call spread width: $165 - $160 = $5.00. Total credit: $2.80 (put) + $2.00 (call) - $1.10 (long call) = $3.70.

Strike validation formula:

Net credit > Call spread width

$3.70 > $5.00? No.

This trade fails the jade lizard test. You need to adjust. Either widen the short strikes (collect more credit), narrow the call spread, or choose a different expiration cycle with higher IV.

Adjusted example:

- Short $138 put at $3.20

- Short $162 call at $2.30

- Long $167 call at $1.00

- Net credit: $3.20 + $2.30 - $1.00 = $4.50

- Call spread width: $167 - $162 = $5.00

- Validation: $4.50 < $5.00? Still no.

Try again:

- Short $138 put at $3.20

- Short $162 call at $2.30

- Long $166 call at $1.10

- Net credit: $4.40

- Call spread width: $4.00

- Validation: $4.40 > $4.00? Yes. This is a valid jade lizard.

Strike selection table:

| Component | Delta | Strike | Premium | Purpose |

|---|---|---|---|---|

| Short put | 0.20–0.30 | 1–2 SD below | $2.50–$4.00 | Primary credit source |

| Short call | 0.15–0.25 | Above current | $1.50–$3.00 | Additional credit |

| Long call | 0.05–0.10 | Further OTM | $0.80–$1.50 | Upside risk cap |

The tighter the call spread, the easier it is to satisfy the credit > width condition, but the less credit you collect from the short call. The wider the call spread, the more credit you can collect, but the harder it is to ensure no upside risk.

Profit zones and risk profile

The jade lizard has three outcome zones at expiration:

Zone 1: Stock finishes above the long call strike

Max profit = net credit received. Both calls are in-the-money. The call spread loses its maximum value (width × 100), but this loss is offset by the credit you collected upfront. Because you built the trade so credit > spread width, you still keep a profit.

Example: Net credit $4.40, call spread width $4.00. Stock finishes at $170. Call spread loses $400. You keep $440 - $400 = $40 profit per contract.

Zone 2: Stock finishes between the short put and short call

Max profit = net credit received. Both the put and the call spread expire worthless. You keep the entire $4.40 credit ($440 per contract).

This is your ideal zone. For a $150 stock with a $138 put and $162 call, you profit fully if the stock finishes anywhere between $138 and $162—a 24-point range, or 16% of the stock price.

Zone 3: Stock finishes below the short put strike

You start losing money. The short put is in-the-money. Max loss = (short put strike - stock price) × 100 - net credit received.

Example: Stock finishes at $130. Short put loses ($138 - $130) × 100 = $800. Net credit received: $440. Total loss: $800 - $440 = $360.

Breakeven = short put strike - net credit = $138 - $4.40 = $133.60.

If the stock finishes below $133.60, you lose money. The further it drops, the worse the loss. Unlike the upside, downside risk is NOT capped by the structure itself—you need to manage it with stop-losses or adjustments.

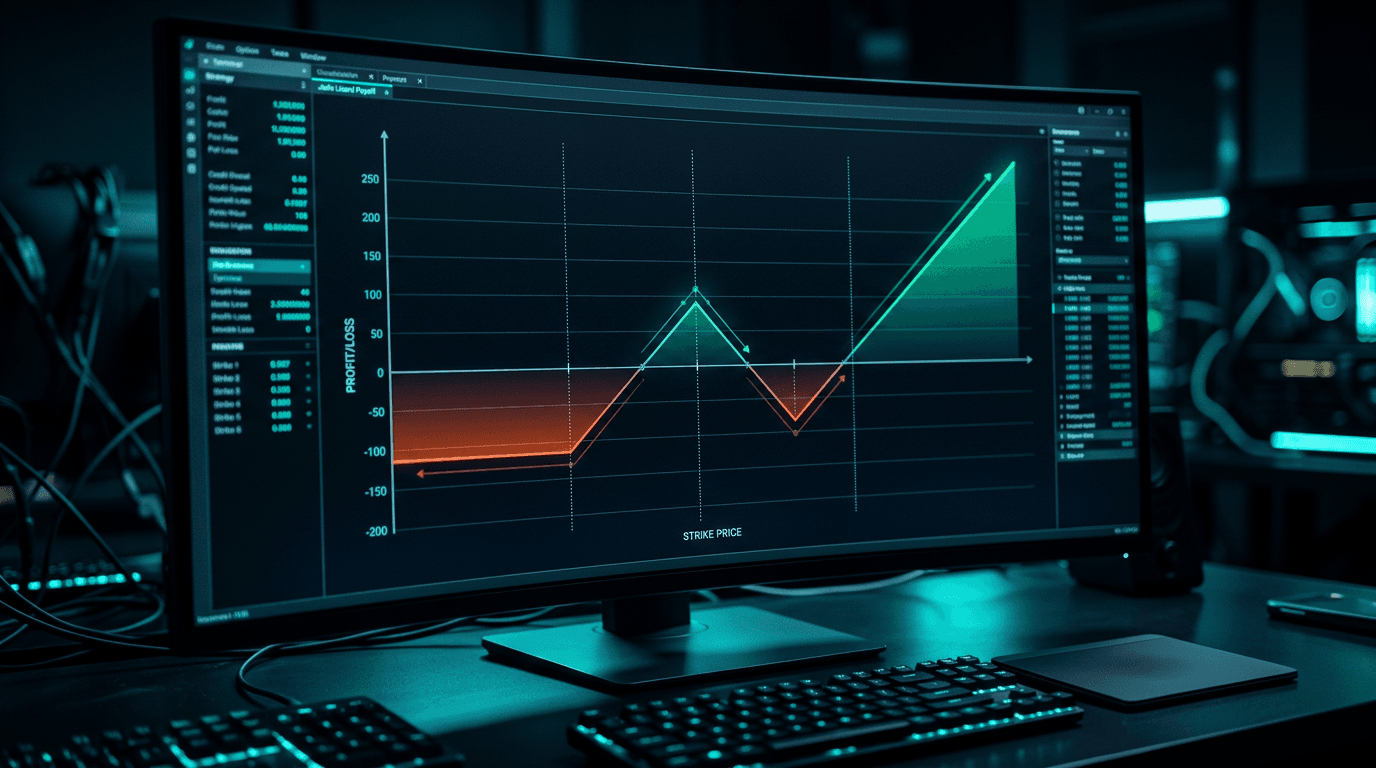

Payoff diagram characteristics:

- Flat profit line from the short call strike to infinity (no upside risk)

- Flat profit line from the short call strike down to the short put strike (max profit zone)

- Diagonal loss line below the short put strike (linear downside risk)

- Breakeven point at short put strike minus net credit

This profile makes the jade lizard a bullish-leaning neutral strategy. You want the stock to stay flat or drift higher, but you can tolerate a moderate pullback down to the breakeven.

Python code: calculating jade lizard payoffs

Here's a Python function to calculate profit/loss at expiration for any stock price, given your three strikes and net credit:

import numpy as np

import matplotlib.pyplot as plt

def jade_lizard_payoff(stock_prices, short_put_strike, short_call_strike, long_call_strike, net_credit):

"""

Calculate jade lizard P&L at expiration.

Parameters:

- stock_prices: array of stock prices at expiration

- short_put_strike: strike of the sold put

- short_call_strike: strike of the sold call

- long_call_strike: strike of the bought call

- net_credit: total credit received (positive number)

Returns:

- Array of P&L values (per contract, in dollars)

"""

payoff = np.zeros_like(stock_prices)

for i, S in enumerate(stock_prices):

# Short put P&L: lose money if S < short_put_strike

put_pl = min(0, S - short_put_strike) * 100

# Call spread P&L: max loss = spread width if S > long_call_strike

if S <= short_call_strike:

call_spread_pl = 0

elif S < long_call_strike:

call_spread_pl = -(S - short_call_strike) * 100

else:

call_spread_pl = -(long_call_strike - short_call_strike) * 100

# Total P&L = credit received + option payoffs

payoff[i] = net_credit * 100 + put_pl + call_spread_pl

return payoff

# Example: $150 stock, 45 DTE

short_put = 138

short_call = 162

long_call = 166

credit = 4.40

stock_range = np.linspace(120, 180, 300)

pl = jade_lizard_payoff(stock_range, short_put, short_call, long_call, credit)

# Find breakeven

breakeven_idx = np.where(np.diff(np.sign(pl)))[0]

if len(breakeven_idx) > 0:

breakeven_price = stock_range[breakeven_idx[0]]

print(f"Breakeven: ${breakeven_price:.2f}")

# Max profit

max_profit = credit * 100

print(f"Max profit: ${max_profit:.2f}")

# Max loss (theoretical, at stock price = 0)

max_loss = (short_put - credit) * 100

print(f"Max loss (at $0): ${max_loss:.2f}")

# Plot

plt.figure(figsize=(10, 6))

plt.plot(stock_range, pl, linewidth=2, color='teal')

plt.axhline(0, color='white', linestyle='--', alpha=0.3)

plt.axvline(short_put, color='red', linestyle='--', alpha=0.5, label='Short put')

plt.axvline(short_call, color='orange', linestyle='--', alpha=0.5, label='Short call')

plt.axvline(long_call, color='green', linestyle='--', alpha=0.5, label='Long call')

plt.xlabel('Stock Price at Expiration')

plt.ylabel('Profit/Loss ($)')

plt.title('Jade Lizard Payoff Diagram')

plt.legend()

plt.grid(alpha=0.2)

plt.show()

Run this with your own strikes and credit to visualize the payoff. The flat top on the right side confirms no upside risk. The diagonal slope on the left shows linear downside risk below the short put.

When to deploy a jade lizard

The jade lizard is not an all-weather strategy. It works best in specific market conditions and stock setups. Deploy it when:

1. Implied volatility is elevated (IV rank > 50)

High IV inflates option premiums, making it easier to collect enough credit to satisfy the spread width condition. If IV is low, you'll struggle to get $4+ in credit without taking on excessive risk. Check IV rank or IV percentile before entering. You want the stock's current IV to be in the top half of its 52-week range. Many options trading platforms integrate AI tools to scan for elevated IV setups—artificial intelligence crypto trading techniques can also be adapted to options screening by filtering for volatility spikes and range-bound price action.

2. You expect the stock to stay neutral or drift higher

The jade lizard is bullish-biased. Your main risk is a sharp drop below the short put. If you think the stock is going to rally hard, sell a naked put instead and collect more premium. If you think it's going to drop, don't trade a jade lizard—use a bear put spread or stay out.

3. The stock is range-bound with support near your short put strike

Look for stocks consolidating after an earnings move, sitting on a key moving average, or trading in a multi-week range. You want technical support below the current price to reduce the odds of a breakdown through your short put.

4. You want income without taking a directional bet

If you're not confident in direction but want to collect premium, the jade lizard offers a wide profit zone. Compare this to selling options for income strategies like covered calls or cash-secured puts, which require you to own shares or commit more capital per contract.

5. You're comfortable managing downside risk

The jade lizard does not cap downside risk. If the stock drops 15%, you're losing money. You need a plan: roll the short put down and out, close the entire position at a loss threshold (e.g., 50% of credit received), or hedge with long puts. If you can't actively manage a losing trade, use an iron condor instead—it caps both upside and downside risk.

Margin requirements and capital efficiency

The margin required for a jade lizard depends on your broker and account type. There are two components:

1. Short put margin

The short put is treated as a naked short option. Margin = 20% of the stock price, minus any out-of-the-money amount, plus the premium received, with a minimum of 10% of the stock price.

Example: $150 stock, $138 short put, $3.20 credit.

- 20% of $150 = $30 per share = $3,000 per contract

- OTM amount: $150 - $138 = $12 per share = $1,200

- Margin = $3,000 - $1,200 + $320 = $2,120 per contract

Some brokers use a simplified formula (e.g., Reg T margin = 20% of stock price per contract = $3,000). Check your broker's margin calculator.

2. Call spread margin

The call spread is a defined-risk vertical spread. Margin = width of the spread × 100 - net credit received from the spread.

Example: $162 short call, $166 long call, net credit from the spread = $2.30 - $1.10 = $1.20.

- Spread width: $4 per share = $400 per contract

- Net credit from spread: $120

- Margin = $400 - $120 = $280 per contract

Total margin for the jade lizard:

Margin = short put margin + call spread margin = $2,120 + $280 = $2,400 per contract.

Compare this to a short strangle (no long call). The strangle requires margin on both the short put and the short call. For the same strikes, the short call would require an additional ~$2,500 in margin, bringing the total to ~$4,600. The jade lizard cuts margin in half while eliminating upside risk.

Capital efficiency table:

| Strategy | Margin per contract | Max profit | Return on margin |

|---|---|---|---|

| Jade lizard | $2,400 | $440 | 18.3% |

| Short strangle | $4,600 | $520 | 11.3% |

| Iron condor | $1,500 | $300 | 20.0% |

| Cash-secured put | $13,800 | $320 | 2.3% |

The jade lizard offers better capital efficiency than a short strangle or cash-secured put, but slightly worse than an iron condor. The tradeoff: the iron condor caps your profit if the stock rallies, while the jade lizard lets you keep the full credit on the upside.

Adjustments: managing the trade when it moves against you

No strategy is set-and-forget. The jade lizard requires active management if the stock moves outside your profit zone. Here are the three most common adjustments:

1. Roll the short put down and out (stock drops toward the short put)

If the stock drops and approaches your short put strike with 2–3 weeks left to expiration, consider rolling the put to a lower strike in a further expiration cycle. This collects additional credit and gives the stock more time to recover.

Example: Stock drops from $150 to $142. Your $138 put is now at-the-money. Roll the $138 put to a $135 put in the next monthly cycle, collecting an additional $1.50 credit. This lowers your breakeven and extends the trade duration.

Risk: You're now in a larger position with more capital at risk. If the stock continues dropping, you'll take a bigger loss.

2. Close the entire position at a loss threshold

Set a stop-loss at 50–100% of the credit received. If the stock breaks below your breakeven, close all three legs and take the loss. Don't let a $400 loss turn into a $1,500 loss because you hoped for a reversal.

Example: You collected $440 credit. The stock drops to $135, and your position is down $600. Close the trade. Your net loss is $600 - $440 = $160.

3. Add a long put to cap downside risk (convert to an iron condor)

If the stock is falling and you want to cap your risk without closing the trade, buy a put below your short put strike. This converts the jade lizard into an iron condor.

Example: Stock at $140, short put at $138. Buy a $133 put for $1.20. Your max loss is now capped at ($138 - $133) × 100 - $440 + $120 = $180.

Tradeoff: You reduce your net credit by the cost of the long put, which lowers your max profit.

Common mistakes that kill jade lizard trades

1. Violating the credit > spread width rule

The defining feature of a jade lizard is no upside risk. If your net credit is less than the call spread width, you have upside risk, and you're just trading a modified short strangle. Always validate: net credit > (long call strike - short call strike).

2. Selling the short put too close to the current price

A delta 0.40 short put might collect $5.00 in credit, but it has a 40% chance of finishing in-the-money. You're taking too much directional risk. Keep the short put delta at 0.25 or lower. Probability of profit should be 70%+ at entry.

3. Ignoring earnings announcements

Never hold a jade lizard through earnings. IV crush will deflate your short options, but the stock can gap past your strikes, turning a high-probability trade into a max-loss scenario. Close the position before earnings or roll it to the post-earnings cycle.

4. Deploying in low IV environments

If IV rank is below 30, premiums are too low to build an efficient jade lizard. You'll either collect insufficient credit or have to widen your strikes so far that your probability of profit drops below 60%. Wait for IV to spike (market selloff, sector volatility, pre-earnings run-up).

5. Not managing winners early

If the stock stays in your profit zone and you've captured 50–70% of the max profit with 2+ weeks to expiration, consider closing the trade. The risk/reward of holding for the last $100 of profit is poor. You're exposed to a surprise gap move for diminishing returns.

Advanced setup: skewing the strikes for directional bias

The standard jade lizard is neutral-to-bullish. You can skew the strikes to express a stronger directional view:

Bullish skew: widen the call spread, tighten the put distance

If you're confident the stock will drift higher, place the short put closer to the current price (delta 0.35) and widen the call spread to collect more credit. This increases your max profit but raises your downside risk.

Example:

- Stock at $150

- Short $145 put (delta 0.35) at $4.00

- Short $162 call at $2.20

- Long $168 call at $1.00

- Net credit: $5.20

- Call spread width: $6.00

- Validation: $5.20 < $6.00. Adjust.

Widen to $170 long call:

- Net credit: $5.50

- Call spread width: $8.00

- Still fails. This shows the limits of bullish skewing—you need elevated IV to make it work.

Neutral skew: equal deltas on the short put and short call

For a true neutral stance, match the delta of the short put and short call (both around 0.20–0.25). This centers the profit zone around the current stock price.

Defensive skew: lower the short put delta, raise the short call delta

If you're worried about downside but still want to collect premium, use a delta 0.15 short put and a delta 0.30 short call. This shifts your profit zone higher but reduces total credit.

The skew you choose depends on your market outlook and risk tolerance. There's no free lunch—more credit means more risk somewhere.

Jade lizard vs other credit strategies

How does the jade lizard compare to similar strategies?

| Strategy | Upside risk | Downside risk | Credit collected | Margin | Best for |

|---|---|---|---|---|---|

| Jade lizard | None | Undefined | High ($4–$6) | Moderate | Neutral-to-bullish, high IV |

| Short strangle | Undefined | Undefined | Highest ($5–$8) | High | Neutral, very high IV, wide ranges |

| Iron condor | Capped | Capped | Moderate ($2–$4) | Low | Neutral, moderate IV, tight ranges |

| Short put | N/A | Undefined | Moderate ($3–$5) | High | Bullish, willing to own stock |

| Call credit spread | None | N/A | Low ($1–$3) | Low | Bearish-to-neutral |

The jade lizard sits between the short strangle and the iron condor. It offers higher credit than an iron condor with no upside risk, but requires more margin and active management than a simple call credit spread.

If you're comparing jade lizards to other multi-leg strategies like the long butterfly option strategy, note that butterflies are debit spreads designed for low-volatility, pinned-stock scenarios, while jade lizards are credit spreads for elevated IV and range-bound movement.

Automating jade lizard entry and exit with AI agents

Manually scanning for jade lizard setups across hundreds of tickers is time-consuming. You need to filter for high IV rank, check technical support levels, validate the credit > spread width condition, and monitor the position for adjustment signals.

An AI agent can automate this entire workflow. Configure an agent in Agentic Traders to scan your watchlist every morning for stocks with IV rank > 60, price above the 50-day moving average, and no earnings in the next 21 days. The agent calculates optimal strikes for a jade lizard, validates the credit condition, and submits the order when criteria are met. If the stock drops within 5% of the short put strike, the agent sends an alert to roll or close the position.

This removes the emotional decision-making and ensures you only enter trades that meet your risk parameters. The agent doesn't guess—it executes the same rules you would manually apply, but across 50 stocks simultaneously.

FAQ

Can you trade a jade lizard in a small account?

Yes, but margin requirements limit position size. A single jade lizard on a $150 stock requires ~$2,400 in margin. In a $10,000 account, you can open 2–3 positions if you're not holding other trades. Use lower-priced stocks ($50–$80) to reduce margin per contract. Some traders use ETFs like SPY or QQQ, but the credit collected is smaller due to tighter bid-ask spreads.

What happens if the stock finishes exactly at the short call strike?

The short call expires at-the-money. You'll likely be assigned, meaning you're short 100 shares at the short call strike. The long call expires worthless (it's out-of-the-money). You now have a short stock position. Most traders close the position before expiration to avoid assignment risk. If you're assigned, buy back the shares immediately or exercise the long call if it's still in-the-money.

How do you close a jade lizard early?

Send a closing order for all three legs simultaneously (buy to close the short put, buy to close the short call, sell to close the long call). This is a multi-leg order. Most brokers support this as a single transaction. If you close the legs individually, you risk legging into a worse fill due to price movement between orders.

Is the jade lizard better than a wheel strategy for income?

Different goals. The wheel strategy (selling options for income by selling puts, getting assigned, then selling calls) is a stock-ownership strategy. The jade lizard is a pure premium-collection strategy with no intention of owning shares. The wheel requires more capital (you need cash to buy 100 shares if assigned). The jade lizard uses margin and can be closed before expiration. Choose based on whether you want to own the underlying stock.

Can you trade jade lizards on weekly options?

Yes, but the credit collected is smaller due to less time value. Weekly jade lizards work best on high-IV, high-beta stocks where weekly premium is still substantial (e.g., TSLA, NVDA, MARA). The tradeoff: you can roll the position more frequently, compounding small gains, but you're also exposed to more gamma risk as expiration approaches.

Putting it together: your jade lizard checklist

Before entering a jade lizard trade, verify:

- IV rank > 50 — premiums are elevated enough to collect sufficient credit

- Net credit > call spread width — no upside risk at expiration

- Short put delta 0.20–0.30 — 70%+ probability the stock stays above the strike

- Short call delta 0.15–0.25 — neutral-to-bullish bias

- No earnings in the next 21 days — avoid IV crush and gap risk

- Technical support near the short put — reduces odds of a breakdown

- Margin available = 2x the required margin — leaves room for adjustments or adding positions

- Exit plan defined — close at 50–70% of max profit, or stop-loss at 100% of credit received

The jade lizard is a high-probability, high-maintenance strategy. It rewards traders who can monitor positions, adjust when needed, and avoid the temptation to "hope" a losing trade will reverse. If you're not willing to manage the downside risk, stick to iron condors or best option trading strategies with defined risk on both sides.

Related articles

- Best Option Trading Strategy: 7 Proven Setups for 2026

- Long Butterfly Option Strategy: Setup, Greeks & Profit Zones

- Selling Options for Income: 7 Strategies That Generate Cash Flow

- Best Covered Calls Stocks: 12 High-Premium Picks for 2026

Test your jade lizard setups with an AI agent that scans for high-IV opportunities and validates strike selection in real time at https://app.agentictraders.io/login.

Continue reading

Option Trading for Beginners: The Complete 2026 Guide (PDF Alternative)

Learn option trading from scratch with real examples, code, and strategy setups. Better than any PDF—actionable, updated for 2026, with automated execution tips.

StrategiesSelling Options for Income: 7 Strategies That Generate Cash Flow

Master selling options for income with premium collection strategies, risk management, and automation. Learn covered calls, cash-secured puts, spreads, and AI execution.

StrategiesLong Butterfly Option Strategy: Setup, Greeks & Profit Zones

Master the long butterfly option strategy with strike selection, breakeven math, and volatility timing. Includes Python code, profit tables, and AI agent configuration.

Platform GuidesBest Option Trading Websites: 7 Platforms Compared for 2026

Compare the best option trading websites for 2026. Real-time Greeks, advanced order types, backtesting, and AI agent integration. Find the platform that fits your strategy.

Run this strategy with an AI agent.

Configure indicators, set rules, paper-trade for free. Your agent watches the charts so you don't have to.

Launch Terminal❯❯❯